Spain Are World Champions: What Great BusinessesCan Learn About Long-Term Investment, Preparation,and Building the Right Foundation

How Spain’s World Cup win mirrors the case for long-term investment in finance systems — and what a well-planned ERP to Xero migration actually looks like. Spain are world champions once again. It’s tempting to focus only on the final whistle. The trophy lift, the celebrations, and the headlines naturally attract the most attention. Yet those moments represent only a small part of the story. Spain won the World Cup because of decisions made years earlier. Coaches, leaders, and administrators invested in academies, training grounds, and long term planning. Those decisions, not any single match, laid the foundation for success. Spanish football didn’t get here by chance. For years, it has invested in youth development, technical excellence, and a clear, consistent playing philosophy. It didn’t build a winning team overnight. It built a system — one that reliably produces world-class talent, tournament after tournament, generation after generation. Businesses face exactly the same challenge, whether they realise it or not. And finance teams, in particular, have a lot to learn from how champions are actually built. This isn’t really an article about football. It’s an article about why the businesses that win — the ones with the fastest month-end close, the clearest reporting, the strongest cash flow, and the calmest finance teams — are rarely the ones working the hardest. They’re the ones working with better systems, built well in advance of when they’re needed. Success Is Never a Single Decision There’s a myth in business that transformation happens in one dramatic moment: the big hire, the big client win, the big software switch. In reality, sustainable success is built from thousands of small, correct decisions made consistently over a long period of time. Spain’s route to the World Cup didn’t hinge on one moment of brilliance. Years of investment in coaching pathways, a clear playing philosophy across every age group, and a culture that valued technical excellence over shortcuts laid the foundation for success. Every pass in the final reflected more than a decade of preparation that most people never saw. Growing businesses work the same way. There is rarely one decision that transforms a company overnight. Instead, success comes from consistently improving every part of the business — including the parts that don’t get much attention until something goes wrong. For finance teams, one of the most overlooked opportunities for this kind of quiet, compounding improvement is the finance system itself. Why “It Still Works” Isn’t a Strategy Many companies delay upgrading their finance systems for a simple reason: the current one still “works.” Invoices go out. Payroll gets processed. The accounts eventually close. Nothing is on fire, so why touch it? But just as Spanish football continually evolved rather than resting on past success, growing businesses need systems that support where they’re heading — not just where they’ve been. An ERP system may have served your business brilliantly for years. But as an organisation grows, the demands on its finance function change, often faster than anyone notices in the moment. Complexity creeps in gradually, and then all at once: None of these arrive as a single crisis. They accumulate. A finance team that was comfortably keeping pace two years ago can suddenly find itself permanently behind, firefighting instead of forecasting — not because anyone did anything wrong, but because the system underneath them never evolved to match the business growing on top of it. This is usually the point at which businesses start looking seriously at Xero, the cloud accounting platform designed to scale with growing organisations. What Legacy Systems Actually Cost You It’s worth being specific about what “the current system still works” actually means in practice, because it rarely means what it sounds like. Many businesses are running legacy ERP systems that have become expensive to maintain, difficult to customize, and increasingly mismatched to their current needs. The system technically functions. But underneath that surface-level functionality, a familiar set of problems tends to build up: None of these show up as a single dramatic failure. They show up as a slow tax on the business — a few extra hours here, a delayed decision there, a report nobody quite trusts. Over time, that tax compounds, in exactly the same way good habits compound in the other direction. What Modern Cloud Accounting Actually Changes Modern cloud accounting has changed what’s realistically possible for finance teams, and the gap between legacy ERP and a modern platform like Xero is now substantial. By migrating from ERP to Xero, businesses typically gain: The benefits extend well beyond the accounting function itself. Businesses that make this move consistently report: Migration Is an Opportunity, Not Just an Upgrade It’s worth being clear about something: migrating from an ERP to Xero isn’t simply changing software. Treated properly, it’s an opportunity to simplify processes, improve visibility, automate manual tasks, and free up a finance team’s time to focus on strategic work rather than administrative firefighting. That distinction matters. A migration done badly just moves the same problems onto a new platform with a nicer interface. A migration done well uses the transition as a genuine reset point — a chance to ask which processes actually still make sense, which reports people actually use, and which approval chains exist for good reason versus historical accident At eCloud Experts, a Xero Gold Champion Partner, ERP to Xero Migration isn’t just about importing data from one system to another. We review your existing finance processes, simplify them where possible, and build your new Xero environment to support long-term growth instead of copying old habits into a new system. Talk to our migration experts today. Because moving systems should improve your business — not just relocate it. Experience Across Every Legacy System We’ve helped businesses migrate from a wide range of legacy ERP and accounting platforms, including: And many more besides. That range matters, because every legacy system carries its own quirks, its own historical workarounds, and its own data structures that need careful handling during ERP

How to Plan a Successful Xero Implementation from Start to Finish

Implementing new accounting software is a significant step for any business. While Xero is known for its user-friendly interface and powerful cloud accounting features, a successful Xero implementation involves much more than simply creating an account and importing your data. A well-planned implementation ensures your financial records remain accurate, your team adapts quickly, and your business continues operating with minimal disruption. Without proper planning, businesses may encounter issues such as incorrect opening balances, duplicate records, reporting errors, or workflow inefficiencies that take time to resolve. Whether you’re moving from Sage, QuickBooks, NetSuite, Zoho Books, spreadsheets, or another accounting system, taking a structured approach will help you get the most from your investment. In this guide, we’ll walk you through every stage of a successful Xero implementation, from planning and preparation to testing, training, and ongoing support. What Is Xero Implementation? Xero implementation is the complete process of setting up Xero so it works effectively for your business. It includes much more than migrating financial data from one system to another. A successful implementation involves reviewing your current accounting processes, preparing and cleaning financial data, configuring Xero, importing records, connecting business applications, testing workflows, training users, and monitoring the system after it goes live. The objective is to create a reliable accounting environment that supports accurate reporting, efficient day-to-day operations, and long-term business growth. Every business has different requirements, so no two implementations are exactly the same. A small business with simple bookkeeping needs will have a different implementation process from a growing company managing inventory, payroll, multiple departments, or international transactions. Why a Well-Planned Xero Implementation Matters Many implementation problems occur because businesses rush the process or underestimate the amount of preparation required. Planning your implementation carefully offers several benefits, including: Instead of simply replacing your accounting software, implementation gives you an opportunity to improve your accounting processes and remove inefficiencies that may have built up over time. Signs Your Business Is Ready for Xero If you’re unsure whether it’s the right time to move to Xero, consider whether any of these situations apply to your business. Recognising these signs early allows you to plan your implementation before accounting issues begin affecting business performance. Benefits of Implementing Xero Businesses choose Xero because it helps simplify financial management while providing access to real-time information. Some of the biggest benefits include: Cloud-Based Access Access your accounts securely from anywhere with an internet connection. Real-Time Financial Reporting View up-to-date financial reports without waiting until month-end. Automated Bank Feeds Reduce manual bookkeeping by importing transactions directly from your bank. Improved Collaboration Multiple users can work in Xero at the same time with role-based permissions. Faster Invoicing Create professional invoices quickly and track payments more efficiently. Integration with Business Apps Connect Xero with hundreds of business applications including payroll, CRM, inventory management, payment platforms, and eCommerce solutions. Set Clear Objectives Before You Begin Every successful Xero implementation starts with a clear understanding of what you want to achieve. Ask yourself: Defining your objectives helps shape the entire implementation project and keeps everyone focused on the same outcomes. Build the Right Implementation Team A successful implementation often involves several people across the business. Team Member Responsibilities Business Owner Approves project decisions and objectives Finance Manager Reviews accounting requirements Accountant Validates financial accuracy Bookkeeper Reviews daily transaction processes IT Support Assists with integrations and access Department Managers Confirm operational workflows Xero Implementation Partner Plans, configures, migrates, tests, and supports the implementation Clear communication throughout the project helps avoid misunderstandings and delays. Review Your Existing Accounting System Before moving to Xero, take time to review your current accounting records. Areas to examine include: Many businesses discover duplicate contacts, unused accounts, or incorrect VAT codes during this review. Cleaning your data before implementation improves reporting accuracy after migration. Decide What Data Should Be Migrated Not every business needs to import years of accounting history. Common migration options include: Opening Balances Only Suitable for businesses beginning a new financial year or those with straightforward reporting requirements. Current Financial Year Provides detailed reporting while keeping implementation relatively simple. Full Historical Transactions Recommended for businesses requiring historical reporting, audits, management analysis, or long-term financial comparisons. Choosing the right migration scope helps balance reporting requirements with implementation time and cost. Prepare Your Financial Data Preparing your financial records is one of the most important parts of any Xero implementation. Before migration, review: Your reports should balance before any data is imported into Xero. Correcting problems beforehand is much easier than resolving them after implementation. Create a Realistic Implementation Timeline Having a structured timeline keeps the project organised and helps avoid unnecessary delays. A typical implementation may look like this: Phase Main Activities Discovery Review current system, define goals, gather requirements Planning Clean data, prepare reports, confirm migration scope Configuration Set up Xero settings, users, VAT, accounts, branding Migration Import financial data and validate records Testing Review reports, workflows, integrations, and permissions Go Live Begin using Xero for daily operations Support Monitor performance and provide additional training Larger organisations may require additional planning depending on complexity. Configure Xero Correctly Proper configuration helps ensure your accounting system supports your business processes from day one. Important setup areas include: Taking time to configure these settings properly reduces the need for future adjustments. Connect Your Business Applications One of Xero’s greatest strengths is its ability to integrate with other software. Popular integrations include: These integrations reduce manual work and improve efficiency across your business. Import Your Financial Data Carefully Importing data should always be completed in stages. Typical data includes: After each import, compare totals against your previous accounting system to ensure accuracy. Protect Your Financial Data During Implementation Financial information is one of your business’s most valuable assets. During implementation, you should: Strong security practices help protect your financial information throughout the project. Test Everything Before Going Live Testing helps identify issues before your team starts using Xero every day. Test areas include: Fixing issues during testing is far easier than correcting live accounting records.

Pressure Creates Diamonds: What England’s World Cup Journey Can Teach Businesses About Performing Under Pressure

Every four years, England embarks on a journey that captures the attention of an entire nation. Pubs fill long before kick-off, workplaces become quieter as employees glance at live scores, and conversations that would normally revolve around business or current affairs suddenly become centred on football. Hope returns with every tournament, and millions of supporters begin to believe that this could finally be England’s moment. For the players, however, the experience is very different. Pulling on the England shirt means carrying more than just personal ambition. It means representing generations of supporters, living up to decades of expectation and performing under the constant scrutiny of one of the world’s most demanding football audiences. Every pass is analysed, every tactical decision debated and every result examined from every possible angle. Very few national teams operate under that level of pressure. Yet despite the expectation, England continues to produce leaders who are prepared to step forward when the stakes are highest. Players such as Harry Kane, Jude Bellingham, Declan Rice and Bukayo Saka understand that pressure is not something to fear. It is simply part of competing at the highest level. Business leaders experience something remarkably similar. While the setting may be different, the emotions are often the same. A Finance Director presenting year-end results to the board, a CEO leading an acquisition, a business owner preparing for external investment or a finance team migrating to a new accounting system all face moments where decisions matter, mistakes are costly and confidence becomes essential. Pressure is not reserved for football stadiums. It exists in every ambitious organisation. The question is never whether pressure will arrive. The real question is whether your business will be ready when it does. Pressure Doesn’t Create Problems—It Reveals Them One of the biggest misconceptions in both football and business is that pressure creates mistakes. In reality, pressure usually exposes weaknesses that already exist. If a football team struggles to keep possession under pressure, the problem did not begin in the knockout stages of the World Cup. It began months earlier on the training ground. Likewise, if a business struggles to produce accurate management reports during an audit or cannot obtain reliable financial information during a period of rapid growth, the underlying issue almost certainly existed long before the pressure arrived. Pressure simply removes the opportunity to hide those weaknesses. This is something we see regularly at eCloud Experts. Businesses rarely decide to modernise their finance systems because everything is running perfectly. More often, growth has highlighted limitations that were previously manageable. Reporting takes longer than it should. Multiple spreadsheets are required to reconcile information. Teams spend more time searching for data than analysing it. Leaders begin making important decisions without having complete confidence in the numbers they are reviewing. The business has not suddenly become inefficient. It has simply reached a point where its existing systems can no longer support its ambitions. That is why finance transformation should never be viewed as a reactive exercise. The strongest organisations invest in better systems before they become absolutely necessary, ensuring they remain confident even when the pressure increases. England’s Success Begins Long Before Kick-Off Supporters only see ninety minutes of football, but international success is built over thousands of hours long before the referee blows the opening whistle. England’s coaching staff analyse opponents in extraordinary detail. Sports scientists monitor physical performance. Analysts review passing patterns, pressing intensity and defensive organisation. Every training session has a clear purpose, and every player understands exactly what is expected of them. None of this guarantees victory. What it does guarantee is preparation. Elite teams understand that preparation gives them the best possible chance of performing when the pressure is greatest. The same philosophy applies to successful businesses. Organisations do not suddenly become efficient during an audit. They do not magically improve financial reporting when investors request additional information, nor do they instantly develop better cash flow visibility during periods of uncertainty. Those capabilities are built over time through disciplined processes, reliable systems and a commitment to continuous improvement. Companies that invest in Cloud Accounting, Finance Transformation and modern reporting tools are not simply upgrading their software. They are creating an environment in which better decisions become possible because accurate information is always available when it matters most. Preparation may not eliminate pressure. But it changes the way organisations respond to it. Leadership Is More Than Scoring Goals When Harry Kane is discussed, the conversation naturally begins with goals. As England’s all-time leading goalscorer, his record speaks for itself. Yet focusing solely on statistics overlooks the qualities that have made him one of the country’s most respected leaders. Kane’s influence extends far beyond the penalty area. He remains composed during difficult moments, accepts responsibility when expectations are highest and consistently leads by example rather than emotion. His calmness under pressure provides confidence for the players around him, allowing the team to remain focused even when momentum shifts. The strongest business leaders demonstrate many of the same characteristics. Great CEOs and Finance Directors do not create panic when challenges arise. Instead, they provide clarity, communicate with confidence and make decisions based on reliable information rather than uncertainty. Their leadership creates stability for everyone around them, enabling teams to remain productive when circumstances become more demanding. That confidence is rarely accidental. It is built on preparation, supported by accurate financial data and strengthened by systems that leaders know they can trust. Strong Foundations Create Confident Organisations England’s recent progress at major tournaments has not been built solely on individual brilliance. While talented players often attract the headlines, their performances are supported by a well-organised team, clear tactical principles and an environment where everyone understands their role. Businesses should aspire to build the same type of foundation. Too many organisations continue to rely on disconnected spreadsheets, outdated accounting software and manual processes that consume valuable time while increasing the risk of errors. Those methods may be sufficient during the early stages of growth, but they become increasingly

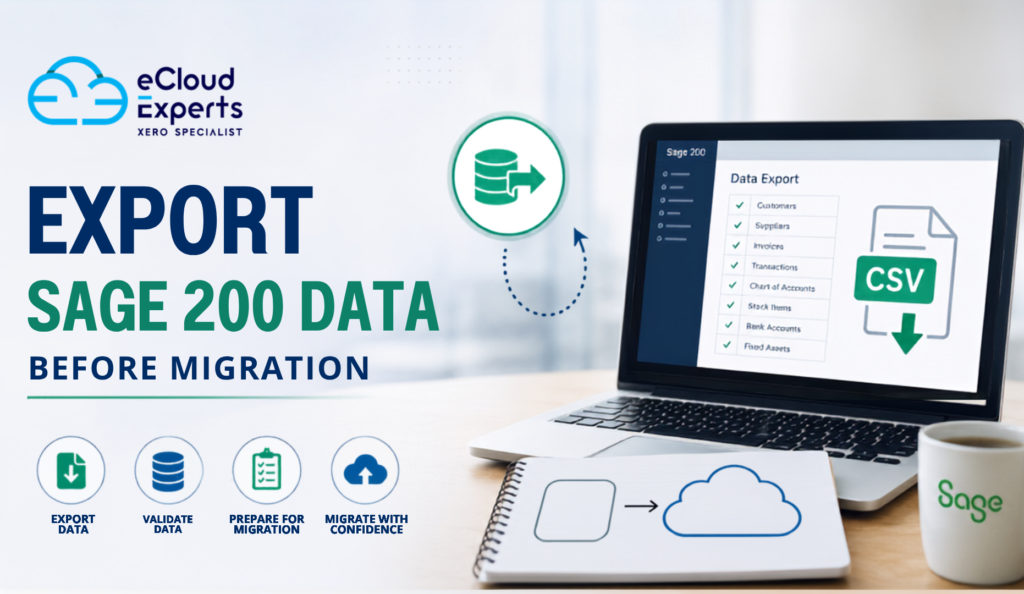

How to Export Sage 200 Data Before Migration: A Complete Step by Step Guide

Migrating from Sage 200 to a modern cloud accounting system is a significant step for any business. Whether you are moving to Xero, QuickBooks Online, or another accounting platform, the quality of your migration depends largely on the quality of the data you transfer. Before any migration can begin, you need to export your Sage 200 data correctly. This process involves much more than downloading a few reports. You must identify which records need to be moved, ensure the data is accurate, and verify that your financial information is complete before importing it into your new system. An incomplete or inaccurate export can result in missing transactions, incorrect opening balances, reporting issues, and unnecessary delays. By taking the time to prepare your data properly, you can reduce migration risks and make the transition much smoother. This guide explains everything you need to know about exporting Sage 200 data before migration, including what to export, how to prepare your records, common mistakes to avoid, and why working with experienced migration specialists can save both time and money. Why Exporting Sage 200 Data Is an Essential Step Every accounting migration begins with data. If the information leaving Sage 200 is incomplete or inaccurate, those same issues will appear in your new accounting software. Exporting your data correctly helps you: A well prepared export provides a solid foundation for your new accounting system and helps ensure the migration is completed successfully. Why Businesses Migrate from Sage 200 Many businesses decide to move away from Sage 200 because their accounting needs have changed. Cloud accounting platforms often provide greater flexibility, easier collaboration, and lower ongoing maintenance costs. Common reasons include: Whatever the reason for migrating, exporting your data correctly is one of the most important parts of the project. When Is the Best Time to Export Sage 200 Data? Timing plays an important role in any migration. Many businesses choose to export their data: Choosing the right time helps minimise disruption and makes financial verification much easier. Prepare Your Sage 200 Data Before Exporting Before creating any export files, spend time reviewing your existing records. Preparation often includes: Remove Duplicate Records Duplicate customers, suppliers, and products can create unnecessary confusion after migration. Review your database carefully and merge or remove duplicates wherever possible. Archive Old Records Inactive customers, discontinued products, and old suppliers may no longer be required. Removing unnecessary information reduces migration complexity and improves system performance. Complete Bank Reconciliations Every bank account should be fully reconciled before exporting. This ensures opening balances match your bank statements after migration. Check Outstanding Transactions Review: Resolving these items beforehand reduces reconciliation work later. Review VAT Records Ensure: This helps maintain accurate tax reporting after migration. What Data Should You Export from Sage 200? A professional migration normally includes several categories of financial and operational data. Chart of Accounts The chart of accounts provides the structure for your financial reporting. Export includes: Customer Information Customer records preserve your sales history and receivables. Typical exports include: Supplier Information Supplier records are equally important. Export includes: Sales Transactions Depending on the migration scope, businesses may export: Purchase Transactions These include: Bank Accounts Exporting bank information helps ensure reconciliation remains accurate. Data may include: VAT Information For UK businesses, VAT is one of the most important areas. Export typically includes: Inventory Inventory businesses usually migrate: Fixed Assets Where applicable, export: Historical Transactions Businesses generally choose one of three options: Your migration specialist can recommend the most suitable approach. How to Export Sage 200 Data Although menu options may vary slightly depending on your Sage 200 version, the overall workflow is similar. Step 1: Back Up Your Sage 200 Database Before exporting anything, create a complete backup of your Sage 200 system. This provides a recovery point if unexpected issues occur. Step 2: Decide What Will Be Migrated Not every business needs every record. Your migration plan should define: Step 3: Generate Export Files Use Sage 200 reporting tools or export utilities to create: These formats can normally be imported into cloud accounting software after appropriate mapping. Step 4: Review the Export Files Check for: Step 5: Validate Financial Reports Before migration begins, compare exported data against Sage reports. Verify: Everything should match before importing into the new system. Common Mistakes When Exporting Sage 200 Data Even experienced users can overlook important details. Exporting Without Cleaning Data Poor quality data leads to poor quality migrations. Always clean your records first. Forgetting Historical Data Businesses sometimes export only current balances, only to realise later they need historical reporting. Plan your reporting requirements in advance. Ignoring Data Validation Always compare exported reports against Sage before migration begins. Incorrect File Formatting Changes to CSV formatting can cause import failures. Avoid editing exported files unless necessary. Missing Custom Fields Some businesses use custom fields that require separate mapping. Review these before migration. Best Practices for Exporting Sage 200 Data Following best practices can significantly improve migration success. These simple steps reduce risk and help ensure a smooth transition. Benefits of Professional Migration Support Although exporting data yourself is possible, professional migration specialists bring valuable experience. They can: This expertise helps reduce downtime and improves confidence throughout the migration. Why Choose eCloud Experts? Migrating accounting systems requires careful planning, technical expertise, and financial accuracy. At eCloud Experts, we have helped businesses across the UK and internationally move from Sage 200 to modern cloud accounting platforms. Our migration service includes: We work closely with every client to ensure their financial data is transferred accurately, allowing them to move to their new accounting system with confidence. Frequently Asked Questions Can I export all my Sage 200 data? Yes. Sage 200 allows you to export financial records, customer and supplier data, invoices, bank transactions, VAT information, inventory, and many other types of business data, depending on your version and configuration. Which export format is best for migration? CSV is the most commonly used format because it is compatible with many accounting systems and migration tools. Excel and

What Brazil’s Attacking Football Can Teach Businesses About Sustainable Growth

“Football is joy.” That’s how many people describe Brazil’s style of play. For decades, Brazil has inspired millions with a philosophy built on creativity, confidence and fearless attacking football. Whether you think of Pelé lifting the Jules Rimet Trophy, Ronaldo Nazário dazzling defenders, Ronaldinho playing with a smile, Kaká gliding through midfield, Neymar producing moments of magic or Vinícius Júnior electrifying the world’s biggest stages, one thing has always remained the same. Brazil doesn’t simply play football. Brazil creates an identity. That identity has delivered five FIFA World Cup titles, produced some of the greatest players in history and inspired generations of football fans around the globe. But here’s something many people overlook. Brazil’s success has never been built on talent alone. Behind every breathtaking goal is meticulous preparation. Behind every famous victory are years of coaching, analysis, discipline and continuous improvement. That’s exactly how successful businesses grow. Many organisations believe growth comes from winning more customers. In reality, sustainable growth comes from building stronger foundations. More sales without stronger systems often lead to more problems. Just as Brazil builds attacks from a solid defensive structure, successful businesses build growth on reliable financial systems. At eCloud Experts, we’ve seen this first-hand. Businesses that invest in modern Cloud Accounting, Finance Transformation and Accounting Software Migration consistently outperform those relying on outdated accounting software, disconnected spreadsheets and manual processes. Technology alone doesn’t create success. The right systems, supported by the right people, do. Brazil Doesn’t Attack Without a Plan To many football supporters, Brazil’s football appears completely natural. A quick passing move. An unexpected dribble. A perfectly timed through ball. A spectacular finish. It looks effortless. But anyone who has played football knows those moments don’t happen by accident. They’re the result of thousands of hours of preparation. Every player understands where they should be. Every movement has a purpose. Business growth follows exactly the same principle. Many companies focus heavily on sales and marketing but neglect the finance systems supporting the business. Initially, growth feels exciting. Revenue increases. New customers arrive. Operations expand. Then problems begin to appear. Growth without strong financial foundations creates unnecessary pressure. That’s why businesses should invest in scalable Cloud Accounting Solutions before growth becomes difficult to manage. Lessons From Brazil’s Greatest Players Every generation has produced Brazilian legends. Pelé demonstrated vision and leadership. Zico showed technical excellence. Ronaldo Nazário combined intelligence with incredible finishing ability. Ronaldinho proved creativity could change games. Kaká inspired through elegance and consistency. Neymar brought flair to a new generation. Today, Vinícius Júnior continues Brazil’s tradition of fearless attacking football. Although every player has a different style, they all share several characteristics. The same characteristics define successful businesses. Markets evolve. Technology changes. Customer expectations increase. Businesses that refuse to adapt eventually fall behind. Those willing to innovate continue growing. Finance leaders should adopt the same mindset. Modern accounting isn’t simply about recording transactions. It’s about creating information that helps leaders make better decisions through accurate Management Reporting and meaningful financial insights. Preparation Creates Confidence Watch Brazil play in a major tournament. Their players rarely panic in possession. Why? Because preparation builds confidence. When you’ve practised something thousands of times, decision-making becomes faster. Businesses experience exactly the same benefit. Companies with accurate financial reporting don’t guess. They know. They know their profitability. They know their cash position. They know which departments are performing well. They know where improvements are needed. Confidence comes from reliable information. Without it, every major decision carries greater risk. That’s one of the biggest reasons organisations invest in Finance Transformation projects—to replace uncertainty with confidence. Growth Is More Than Increasing Revenue Many people define growth as higher sales. That’s only part of the story. Real business growth means: Revenue without financial control isn’t sustainable. Brazil understands this in football. Beautiful attacking football only succeeds because every player understands their responsibilities. Business works exactly the same way. Sales. Operations. Finance. Marketing. Customer service. Leadership. Every department must work together. When finance provides accurate, real-time information, every other team performs better. That’s why finance should never be viewed as a back-office function. It should be viewed as one of the most important competitive advantages a business can have. At eCloud Experts, we help businesses unlock that advantage through Finance Transformation, Cloud Accounting and Accounting Software Migration. Every World-Class Team Uses Data Football has changed dramatically over the last two decades. While Brazil will always be known for its flair and attacking football, today’s success is driven by far more than individual brilliance. Modern football is powered by data. Every sprint is tracked. Every pass is analysed. Every shot is measured. Every player’s workload is monitored to reduce injuries and maximise performance. Managers and coaching staff use advanced analytics to identify strengths, expose weaknesses and make better tactical decisions. The world’s biggest clubs and international teams invest millions in performance analysis because they understand one simple truth: Better information leads to better decisions. Business leaders should adopt exactly the same philosophy. Instead of relying on assumptions, organisations should rely on accurate financial information to guide every important decision. That’s why businesses increasingly invest in Finance Transformation—giving leadership teams access to reliable data instead of outdated reports. From Match Statistics to Financial Reporting Imagine Brazil’s coaching staff preparing for a World Cup match without knowing: It would be almost impossible to compete against the world’s best teams. Now consider your own business. Could you answer these questions today? If those answers aren’t immediately available, your business could be making important decisions with incomplete information. Modern Management Reporting provides the visibility every leadership team needs to make confident decisions. Technology Wins Championships Brazil has always embraced innovation. Today’s players train using GPS technology, video analysis, sports science and AI-driven performance insights. Technology hasn’t replaced coaching. It has made coaching more effective. The same applies to finance. Modern organisations are replacing manual processes with intelligent automation, allowing finance professionals to spend less time entering data and more time delivering valuable business insights. Cloud technology

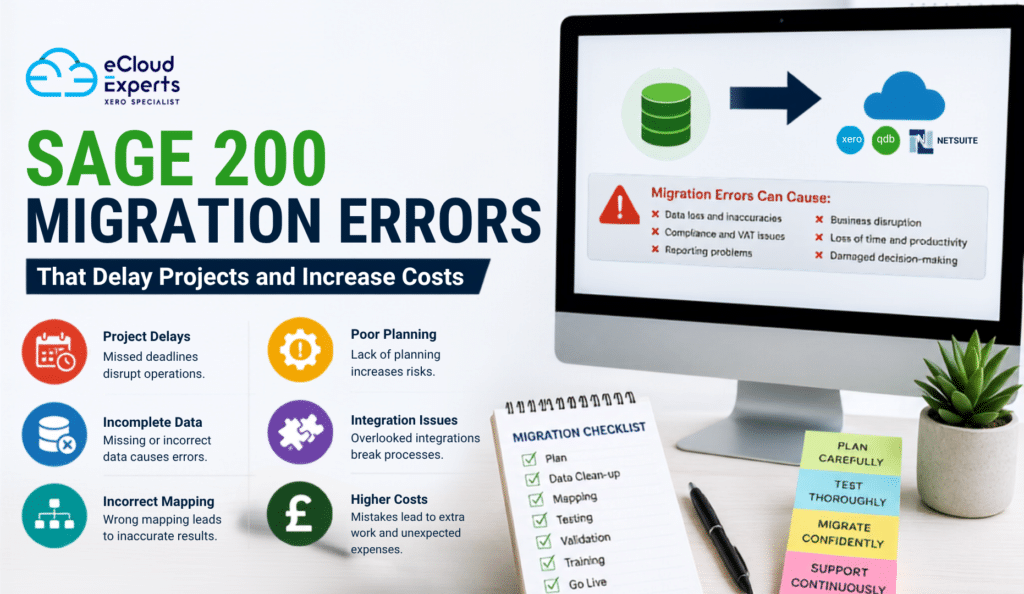

Sage 200 Migration Errors That Delay Projects and Increase Costs

Migrating from Sage 200 to a modern cloud accounting platform is a major step for any business. Whether you are moving to Xero, QuickBooks Online, NetSuite, or another cloud solution, a successful migration can improve reporting, automate everyday tasks, strengthen collaboration, and provide better visibility into your finances. However, many businesses underestimate the complexity of a migration project. They often assume it is simply a matter of exporting data from Sage 200 and importing it into a new system. In reality, a migration involves planning, data preparation, validation, testing, user training, and ongoing support. Making mistakes during any of these stages can delay your project, increase costs, and create accounting issues that take weeks or even months to resolve. The good news is that most Sage 200 migration errors are completely avoidable. With the right preparation and guidance, businesses can complete their migration smoothly while protecting the accuracy of their financial data. In this guide, we explain the most common Sage 200 migration mistakes, why they happen, and how to avoid them. Why Sage 200 Migration Projects Fail A migration project affects much more than your accounting software. It impacts your finance team, management, reporting, sales processes, purchasing, inventory, payroll, and business operations. When projects are rushed or poorly planned, small issues can quickly become expensive problems. Some common consequences include: Understanding these risks before your migration begins can save both time and money. 1. Starting Without a Proper Migration Strategy One of the biggest Sage 200 migration errors is beginning the project without a detailed migration plan. Many businesses focus on choosing new software but spend very little time planning how the migration will actually happen. A migration strategy should include: Without clear planning, teams often experience confusion, duplicated work, and unexpected delays. How to avoid this mistake Create a detailed migration roadmap before any data is transferred. Define milestones, assign responsibilities, and allow enough time for testing and user training. 2. Migrating Poor Quality Data Cloud accounting software is only as good as the data inside it. Many businesses migrate years of duplicate customers, inactive suppliers, incorrect account codes, and outdated records simply because they never cleaned the database. This creates unnecessary problems in the new system, including: Migrating poor quality data simply transfers old problems into a new environment. How to avoid this mistake Review your Sage 200 database before migration. Archive unused records, remove duplicates, correct errors, and ensure your chart of accounts is organised. 3. Choosing the Wrong Migration Date Timing plays a major role in every migration project. Many businesses schedule migrations during their busiest financial periods, creating unnecessary pressure on employees. Avoid migrating during: Trying to manage both daily operations and a migration at the same time often leads to mistakes. How to avoid this mistake Choose a quieter period whenever possible. Many organisations migrate over weekends or during holiday periods to minimise disruption. 4. Not Defining the Migration Scope Another common Sage 200 migration error is failing to define exactly what information should be migrated. Some businesses migrate far more data than they actually need. Others migrate too little and later realise important information is missing. Typical migration data includes: How to avoid this mistake Agree on the migration scope before the project begins. Your migration partner should explain exactly what will and will not be transferred. 5. Ignoring Data Mapping Every accounting system stores information differently. One of the most overlooked Sage 200 migration errors is incorrect data mapping. Examples include: Poor mapping often results in inaccurate reports after migration. How to avoid this mistake Carefully review mapping documents before migration begins and verify that every important field has been matched correctly. 6. Forgetting About Integrations Many businesses use Sage 200 alongside other business software. Examples include: Ignoring these integrations can interrupt everyday operations after migration. How to avoid this mistake Create a complete list of connected applications and check whether each integration is compatible with your new accounting software. 7. Overlooking Custom Reports and Workflows Many Sage 200 systems have been customized over several years. Your business may rely on: These features may not exist in your new software without additional setup. How to avoid this mistake Review every custom process before migration and identify suitable alternatives where necessary. 8. Skipping Data Validation Some businesses believe the migration is complete once the data has been imported. In reality, validation is one of the most important parts of the project. Every migration should compare: Without proper validation, errors may remain hidden until much later. How to avoid this mistake Carry out detailed reconciliation between Sage 200 and the new system before going live. 9. Not Testing Before Go Live Testing allows businesses to identify issues before employees begin using the new software. Skipping this stage can result in: Testing reduces risk and improves confidence. How to avoid this mistake Complete User Acceptance Testing (UAT) using real business scenarios before final migration. 10. Failing to Back Up Sage 200 Although professional migrations are carefully managed, unexpected issues can occur. Without a secure backup, recovering lost information becomes much more difficult. How to avoid this mistake Create multiple secure backups before any migration work begins and store them safely until the project is complete. 11. Poor Communication Throughout the Project Migration projects involve finance teams, managers, business owners, and external partners. When communication is poor, misunderstandings become common. Employees may not know: This creates confusion and slows adoption. How to avoid this mistake Provide regular updates throughout the project and involve key stakeholders from the beginning. 12. Skipping Staff Training A successful migration does not end when data has been transferred. Employees need confidence using the new software. Without training, businesses often experience: How to avoid this mistake Deliver role specific training before and after go live to help users adapt quickly. 13. Underestimating Historical Data Requirements Many businesses only realise after migration that they still need access to historical transactions for reporting, audits, or compliance. This can result in additional work

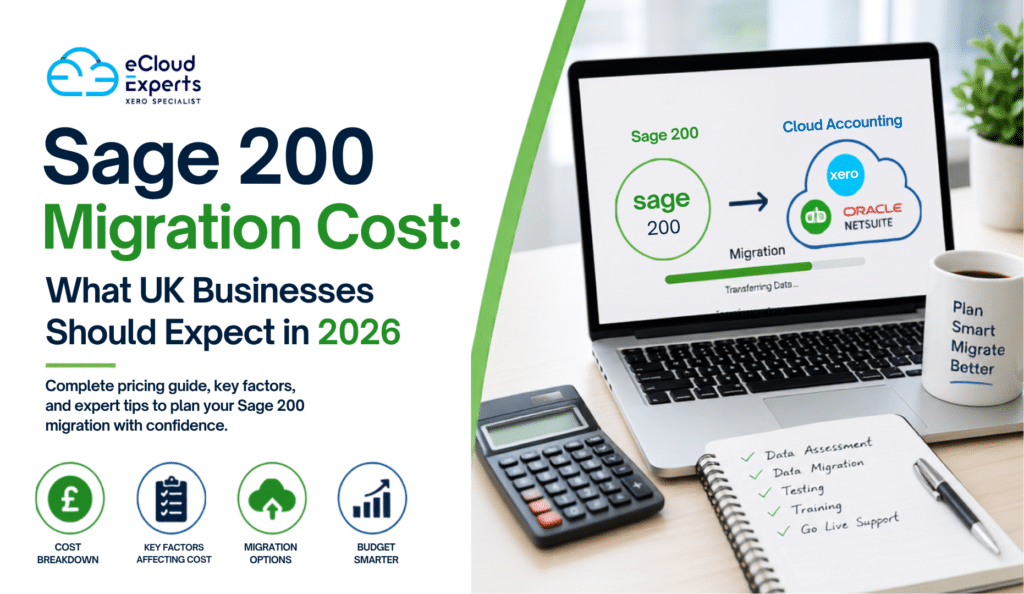

Sage 200 Migration Cost: What UK Businesses Should Expect in 2026

Many UK businesses are reviewing their accounting systems in 2026. Rising software costs, changing business needs, and the demand for better cloud access are encouraging companies to move away from older systems and adopt modern accounting platforms. The answer depends on several factors, including the size of your business, the complexity of your data, and the accounting platform you are moving to. While some migrations can be completed for a few thousand pounds, larger projects involving multiple departments, integrations, and years of historical data can require a more significant investment. Understanding Sage 200 migration cost before starting a project helps businesses budget effectively, avoid surprises, and choose the right migration partner. In this guide, we will explore the factors that influence Sage 200 migration cost, typical price ranges in the UK, hidden expenses to consider, and practical ways to reduce costs while ensuring a successful migration. Thinking about moving from Sage 200? Understanding the true Sage 200 migration cost is the first step toward a successful transition. Get a tailored migration estimate from eCloud Experts and discover how much your business could save with the right cloud accounting solution. Why UK Businesses Are Moving Away from Sage 200 Sage 200 has served businesses well for many years. It offers strong accounting functionality and business management tools. However, the business software landscape has changed significantly. Many companies now prefer cloud accounting platforms because they provide greater flexibility and accessibility. Common reasons businesses move away from Sage 200 include: As businesses explore cloud alternatives, researching Sage 200 migration cost becomes an important part of the decision making process. What Is a Sage 200 Migration? A Sage 200 migration involves transferring financial and operational data from Sage 200 to another accounting or ERP system. Depending on business requirements, this may include: A professional migration also includes planning, validation, testing, and support to ensure data accuracy. Understanding what is included helps businesses evaluate the true Sage 200 migration cost rather than comparing quotes based only on data transfer. Average Sage 200 Migration Cost in 2026 Every project is unique, but most UK businesses fall into one of three categories. Basic Migration Typical cost: £1,500 to £3,500 Usually includes: This option is often suitable for small businesses with straightforward accounting requirements. Standard Migration Typical cost: £3,500 to £8,000 Usually includes: Many growing businesses fall into this category. Advanced Migration Typical cost: £8,000 to £20,000 or more Usually includes: These projects often involve larger organizations with sophisticated accounting processes. The Biggest Factors Affecting Sage 200 Migration Cost Not all migrations are created equal. Several key factors directly influence pricing. Volume of Historical Data One of the largest drivers of Sage 200 migration cost is the amount of historical data being transferred. For example: The more historical data you need, the more time migration specialists must spend extracting, cleaning, validating, and importing records. Transaction Complexity Businesses with thousands of transactions generally face higher migration costs. Complex transactions may include: Each additional layer of complexity increases project effort and affects overall Sage 200 migration cost. Chart of Accounts Structure Many Sage 200 users have customized charts of accounts over the years. Migration specialists must: A complicated account structure can significantly increase migration time. Inventory Requirements Inventory migration often requires additional work. Businesses may need to migrate: Companies with large inventories should expect inventory requirements to increase Sage 200 migration cost. Number of Users Larger teams often require: These additional services contribute to the overall project budget. How Integrations Affect Cost Many businesses use Sage 200 alongside other software. Common integrations include: When migrating to a new platform, these integrations may need to be rebuilt or reconfigured. This often represents a significant portion of total Sage 200 migration cost. For some businesses, integration work can cost as much as the migration itself. Sage 200 to Xero Migration Cost Xero remains one of the most popular destinations for Sage 200 users. Businesses are attracted by: Typical pricing includes: Business Size Typical Cost Small Business £1,500 to £4,000 Medium Business £4,000 to £8,000 Complex Business £8,000 to £15,000+ The final Sage 200 migration cost depends on data volume and customization requirements. Sage 200 to QuickBooks Online Migration Cost QuickBooks Online is another popular option. Businesses often choose it because of: Typical migration costs include: Again, the exact Sage 200 migration cost depends on project scope. Sage 200 to NetSuite Migration Cost Some organizations require a more advanced ERP solution. NetSuite offers: Because implementations are more extensive, costs are generally higher. Typical ranges include: Businesses should view these projects as strategic investments rather than simple software migrations. Hidden Costs Businesses Often Miss When estimating Sage 200 migration cost, many businesses focus only on migration fees. However, several additional costs may arise. Staff Training Employees need time to learn the new system. Training costs may include: Without training, users may struggle to adopt the new platform effectively. Data Cleanup Many Sage 200 systems contain outdated information. Examples include: Cleaning this data improves migration quality but can add additional costs. Custom Reports Custom reports rarely transfer automatically. Businesses may need to recreate: This work can increase overall Sage 200 migration cost. Downtime Planning Some migrations require planned downtime. Businesses may need to allocate resources to: Proper planning helps reduce disruption. How to Reduce Sage 200 Migration Cost The good news is that businesses can take several steps to control migration expenses. Remove Unnecessary Data Not every record needs to be migrated. Removing unnecessary data reduces project complexity. Focus on: Define Clear Objectives Many migration projects become expensive because requirements change during implementation. Create a detailed migration plan before work begins. Identify: A clear scope helps control Sage 200 migration cost. Archive Historical Data Some businesses choose to archive older records instead of migrating everything. This approach often reduces costs significantly. Choose an Experienced Migration Partner Experienced specialists can identify issues early and avoid costly mistakes. While their fees may be higher initially, they often save money overall through efficiency and accuracy. Why the

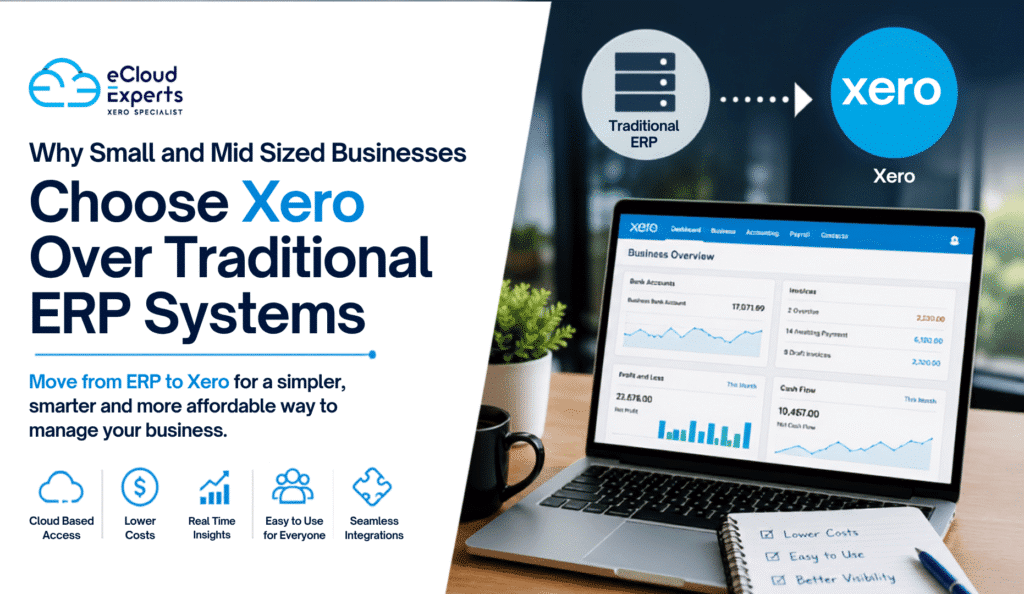

Why Small and Mid Sized Businesses Choose Xero Over Traditional ERP Systems

Running a business today is very different from how it was ten years ago. Companies need real time financial information, remote access, faster reporting, and systems that support growth without creating unnecessary complexity. For many small and mid sized businesses, traditional ERP systems once seemed like the obvious choice. They offered extensive functionality and enterprise level features. However, as technology has evolved, many businesses have started questioning whether they truly need large, expensive ERP platforms. As a result, more organizations are deciding to move from ERP to Xero. They are discovering that cloud accounting software can provide the tools they need without the high costs, long implementation times, and complicated processes associated with traditional ERP systems. In this guide, we will explore why businesses are making the decision to move from ERP to Xero, what benefits they gain, and how a successful migration can support future growth. Understanding Traditional ERP Systems Enterprise Resource Planning systems, commonly known as ERP systems, are designed to manage multiple business functions within a single platform. These systems often include: Popular ERP platforms include: While these systems offer powerful functionality, they can also become expensive and difficult to manage, especially for growing small and mid sized businesses. Why Businesses Decide to Move from ERP to Xero Many business owners initially invest in ERP software because they expect it to support future growth. However, after several years, they often discover that: This is where the decision to move from ERP to Xero begins to make sense. Rather than paying for features they rarely use, businesses can focus on a simpler, cloud based solution that delivers what they actually need. Lower Software Costs One of the biggest reasons companies choose to move from ERP to Xero is cost reduction. Traditional ERP systems often involve: These expenses can quickly add up. Xero operates on a subscription model that offers predictable monthly pricing. Businesses know exactly what they are paying each month without worrying about large upgrade bills or infrastructure costs. For many companies, the savings achieved after they move from ERP to Xero can be substantial. Easier to Use Many ERP systems were designed for large organizations with dedicated finance departments. As a result, they often include: For smaller businesses, this complexity can create frustration. Xero focuses on simplicity. Its clean interface allows users to: without extensive training. This ease of use is a major reason businesses continue to move from ERP to Xero. Faster Access to Financial Information Business owners need accurate financial information quickly. Traditional ERP systems can sometimes require: Xero provides real time dashboards that display: This immediate visibility helps management make faster decisions. Companies that move from ERP to Xero often report significant improvements in financial transparency. Cloud Based Accessibility The modern workforce is increasingly mobile. Employees work from: Traditional ERP systems may require: Xero is fully cloud based. Users can securely access financial data from virtually anywhere with an internet connection. This flexibility is another reason organizations choose to move from ERP to Xero. Reduced IT Requirements Maintaining ERP infrastructure can become a significant burden. Businesses may need: With Xero, these responsibilities are greatly reduced. The platform handles: As a result, companies that move from ERP to Xero often reduce both IT costs and administrative workload. Faster Implementation ERP implementations can take months or even years. Common challenges include: In contrast, Xero deployments are generally much faster. After businesses move from ERP to Xero, they can often begin using the platform within weeks rather than months. This faster implementation allows organizations to focus on running their business rather than managing software projects. Better Integration with Modern Business Apps Today’s businesses rely on specialized software for different functions. Examples include: Xero integrates with hundreds of business applications. Popular integrations include: Businesses that move from ERP to Xero often discover that these integrations improve efficiency and reduce manual work. Improved Collaboration with Accountants Accountants and bookkeepers increasingly prefer cloud based systems. Traditional ERP environments can create challenges when external advisors need access. With Xero: This improved collaboration is another factor encouraging businesses to move from ERP to Xero. Scalability Without Complexity Many organizations worry that moving away from ERP systems may limit growth. In reality, Xero supports thousands of growing businesses worldwide. As businesses expand, they can add: This allows companies to scale without maintaining an overly complex ERP environment. That is why many growing organizations continue to move from ERP to Xero even as revenue increases. Better User Adoption A software system only delivers value if employees actually use it. ERP platforms often suffer from: Xero’s intuitive design helps employees become productive more quickly. Higher adoption rates mean businesses gain greater value from their accounting software investment. This is another practical reason businesses decide to move from ERP to Xero. Common ERP Systems Businesses Replace with Xero Organizations frequently migrate from: NetSuite to Xero Companies seeking lower costs and simpler accounting workflows often move away from NetSuite. Sage ERP to Xero Many businesses want a modern cloud platform with easier access and reporting. Microsoft Dynamics to Xero Smaller organizations sometimes find Dynamics more complex than necessary for their needs. Acumatica to Xero Businesses looking to simplify operations often choose Xero as a more user friendly alternative. SAP Business One to Xero Growing companies may decide that SAP’s extensive functionality exceeds their current requirements. Key Considerations Before You Move from ERP to Xero Before starting a migration project, businesses should evaluate: Historical Data Requirements Determine how many years of data need to be migrated. Chart of Accounts Structure Review account codes and reporting requirements. Customer and Supplier Records Ensure contact information is clean and accurate. Open Transactions Identify outstanding invoices, bills, and balances. Reporting Needs Confirm that required reports can be recreated within Xero. Integration Requirements Review all connected applications before migration. Proper planning helps ensure a successful transition. How eCloud Experts Helps Businesses Move from ERP to Xero At eCloud Experts, we help businesses safely move from ERP to Xero with minimal disruption.

Sage to Xero Migration Cost in the UK: What Businesses Should Expect in 2026

Many UK businesses are rethinking their accounting systems in 2026. Some want better visibility into their finances. Others are looking for improved automation, easier collaboration with accountants, or greater flexibility through cloud accounting. As a result, more businesses are moving from Sage to Xero. Before making the switch, however, one important question usually comes first: What is the Sage to Xero migration cost UK businesses should expect in 2026? The answer depends on several factors. The size of your business, the amount of data being transferred, the complexity of your accounts, and the level of support you require can all influence the final cost. Some businesses spend only a few hundred pounds on a simple migration. Others invest several thousand pounds for a complete migration that includes years of historical data, inventory records, payroll information, and post migration support. This guide explains everything you need to know about Sage to Xero migration cost UK services, helping you budget effectively and avoid surprises during the migration process. Thinking about switching from Sage to Xero? Get expert support and a tailored migration plan from eCloud Experts today. Why More UK Businesses Are Switching from Sage to Xero Accounting software has evolved significantly over the past decade. While Sage remains a well known accounting solution, many businesses are now prioritising cloud based platforms that provide greater accessibility and automation. Xero has become one of the leading cloud accounting systems because it offers: For many companies, these advantages justify the investment involved in a migration project. When businesses evaluate the Sage to Xero migration cost UK, they often compare it against the potential long term benefits of moving to a modern cloud accounting platform. What Does a Sage to Xero Migration Actually Involve? Many business owners assume that migration simply means exporting data from Sage and importing it into Xero. In reality, the process is much more detailed. A successful migration typically includes: Every step plays a role in ensuring the accuracy of your financial information. Skipping any of these stages can lead to reporting issues, reconciliation problems, or incorrect VAT submissions later. Factors That Affect Sage to Xero Migration Cost UK No two migrations are identical. Several factors influence how much businesses ultimately pay. Volume of Historical Data One of the biggest cost drivers is the amount of historical data being migrated. Some businesses choose to transfer only opening balances. Others want: The more history you transfer, the more time is required for extraction, validation, and testing. This often increases the overall Sage to Xero migration cost UK businesses receive. Number of Transactions Transaction volume also affects pricing. A business processing 500 transactions per month requires far less work than one processing 20,000 transactions monthly. Larger transaction volumes usually require: Consequently, businesses with high transaction volumes generally face higher migration costs. Complexity of Business Operations Every business uses accounting software differently. A simple consultancy business may have a straightforward chart of accounts and limited transaction types. Larger businesses may have: More complexity means more planning, testing, and verification. As complexity increases, so does the Sage to Xero migration cost UK. Data Quality One factor many businesses overlook is data quality. During migration planning, providers often discover: Cleaning these issues takes additional time. However, resolving them before migration usually leads to better results and cleaner reporting in Xero. Typical Sage to Xero Migration Cost UK Businesses Can Expect in 2026 While costs vary significantly, the following estimates provide a useful benchmark. Migration Type Estimated Cost Opening balances only £300 to £800 Basic migration £800 to £1,500 Standard migration with transaction history £1,500 to £3,000 Full historical migration £3,000 to £5,000 Complex enterprise migration £5,000+ These figures are intended as general guidelines. The actual Sage to Xero migration cost UK for your business will depend on your specific requirements. What Is Usually Included in a Migration Service? Comparing migration quotes can be difficult because providers include different services. Understanding what is included is often more important than simply choosing the cheapest option. Initial Consultation The migration provider reviews your requirements and discusses project goals. This stage helps determine: Data Assessment Your Sage data is analysed before migration begins. This allows specialists to identify: Data Extraction Financial records are securely extracted from Sage. Data Mapping Information from Sage must be correctly matched to Xero fields. Examples include: Data Import The prepared data is imported into Xero using approved migration procedures. Validation and Reconciliation This stage ensures balances match between both systems. Key areas checked include: User Training Many providers include introductory Xero training. This helps staff become comfortable with the new system quickly. Post Migration Support Support after migration can be invaluable. Users often have questions during the first few weeks of using Xero. Hidden Costs Businesses Should Watch For One of the most common mistakes businesses make is focusing only on the headline price. Some migration quotes exclude important services. Data Cleanup Charges Poor quality data often requires additional work before migration. Payroll Migration Fees Payroll information may require separate processing. Inventory Migration Costs Inventory records can be complex and often involve additional charges. Additional Historical Data Extra years of transaction history may increase pricing. Training Fees Not all migration providers include staff training. Custom Reporting Setup Businesses requiring specialised reports may incur additional costs. Always request a detailed breakdown before approving a migration proposal. DIY Migration vs Professional Migration Many business owners wonder whether they can save money by migrating themselves. The answer depends on the complexity of the business. DIY Migration Advantages DIY Migration Disadvantages Professional Migration Advantages Professional Migration Disadvantages For many businesses, the reduced risk alone makes professional migration worthwhile. How Long Does a Sage to Xero Migration Take? Migration timelines vary based on complexity. Typical projects take: Business Type Typical Timeline Small business 1 to 2 weeks Medium business 2 to 4 weeks Large business 4 to 8 weeks Enterprise project 8+ weeks Businesses often schedule migrations around: Proper planning helps minimise disruption. Ways to Reduce Sage to Xero

Xero Cleanup Case Study: How eCloud Experts Helped Little Spring Wonders Daycare Nursery Restore Confidence in Their Financial Data

Client Overview Little Spring Wonders Daycare Nursery Limited is a growing childcare provider that relies on accurate financial information to manage cash flow, monitor performance, and support business decisions. Like many growing businesses, day-to-day operational demands meant that bookkeeping processes had evolved over time, resulting in historical reconciliation issues and uncertainty around the accuracy of financial reports. To ensure that Xero could be relied upon as the single source of truth, the directors engaged eCloud Experts to perform a comprehensive Xero Cleanup, Xero Health Check, and Xero Optimisation review. Project Summary Client: Little Spring Wonders Daycare Nursery Limited Industry: Childcare & Nursery Services Software: Xero Project Type: Xero Cleanup & Optimisation Review Period: 1 November 2024 to 31 January 2026 Delivered By: eCloud Experts Services Provided Xero Cleanup Service Xero Health Check Xero Reconciliation Service Xero Bookkeeping Review Xero Optimisation Bank Balance Verification Transaction Corrections Bank Rule Creation Workflow Review Add-On Recommendations The Challenge The management team wanted confidence that the financial information held within Xero was accurate and that the reports being used to make business decisions could be relied upon. Several areas required investigation, including: Bank balances requiring verification. Historical unreconciled transactions. Transactions requiring correction or reallocation. Inefficient reconciliation processes. Opportunities to automate recurring bookkeeping tasks. Need for improved bookkeeping controls and workflows. The objective was not simply to reconcile transactions but to ensure that Xero was operating efficiently and producing reliable financial information. What We Found During our Xero Health Check, we identified several areas that required attention. Historical Reconciliation Issues A number of bank transactions had not been fully reconciled, creating differences between bank activity and accounting records. Inconsistent Transaction Processing Some transactions required further investigation to determine whether they had been posted correctly and whether they should be amended, deleted, or recreated. Opportunities for Automation Recurring transactions that were being processed manually could be automated through bank rules and improved workflows. Process Improvement Opportunities The existing setup presented opportunities to streamline bookkeeping procedures and improve reporting accuracy. While these issues are common in growing businesses, left unresolved they can lead to unreliable reports, inefficient bookkeeping, and reduced confidence in financial data. The eCloud Experts Solution Step 1: Bank Balance Verification We reviewed the bank balances recorded in Xero and compared them against actual bank statements covering the entire review period from 1 November 2024 to 31 January 2026. Where differences were identified, we investigated the root cause and implemented corrective actions. Step 2: Full Bank Reconciliation Our team reviewed and reconciled all bank transactions within the project period. This included: Reviewing historical reconciliations. Identifying missing transactions. Resolving discrepancies. Ensuring bank balances accurately reflected real-world balances. Step 3: Transaction Cleanup Where transactions were identified as inaccurate or incorrectly processed, we reviewed whether they should be: Corrected. Reallocated. Deleted. Recreated. This process helped improve reporting accuracy and financial reliability. Step 4: Bank Rule Creation To improve future efficiency, we created bank rules where appropriate. This reduced manual data entry and simplified future reconciliation processes. Step 5: Xero Optimisation Review We carried out a broader review of the Xero environment to identify opportunities for improvement, including: Reconciliation workflows. Bookkeeping procedures. Reporting structure. Coding consistency. System configuration. Step 6: Add-On Recommendations We also provided recommendations for cloud applications and integrations that could help automate finance processes and improve operational efficiency. Results The project provided Little Spring Wonders Daycare Nursery Limited with a cleaner, more reliable, and better-structured Xero environment. Key Outcomes ✅ Bank balances reviewed and matched ✅ Historical bank transactions reconciled ✅ Transaction discrepancies identified and corrected ✅ Improved bookkeeping accuracy ✅ Bank rules implemented where appropriate ✅ Xero setup reviewed and optimised ✅ Recommendations provided for future efficiency improvements ✅ Improved confidence in management reporting Business Benefits More Reliable Financial Reports Management can now make decisions with greater confidence, knowing that the underlying financial information is accurate and up to date. Faster Bank Reconciliations Improved processes and bank rules reduce the time required to reconcile future transactions. Better Financial Visibility Clean and accurate records provide a clearer picture of business performance and cash flow. Improved Internal Controls The review highlighted opportunities to strengthen bookkeeping procedures and reduce the risk of future errors. Greater Efficiency By optimising Xero and introducing automation where appropriate, the business can spend less time on administration and more time focusing on growth. Expert Insight: Why Xero Cleanup Projects Matter One of the most common misconceptions we encounter is that Xero reporting issues are caused by software limitations. In reality, most problems originate from: Incorrect transaction coding. Unreconciled bank transactions. Duplicate entries. Inconsistent bookkeeping procedures. Lack of automation. A structured Xero Cleanup and Health Check can often uncover issues that have accumulated over months or even years. Businesses that perform regular Xero reviews typically experience: More accurate reporting. Faster month-end processes. Improved bookkeeping efficiency. Better cash flow visibility. Greater confidence in financial data. Client Feedback “We engaged eCloud Experts to review and clean up our Xero account, as we wanted confidence in the accuracy of our financial records and bank reconciliations. The team carried out a detailed review of our accounts, reconciled historical transactions, identified areas that required correction, and provided practical recommendations to improve the way we use Xero going forward. Their work has given us greater confidence in our financial data and helped establish a stronger foundation for future bookkeeping and reporting. We particularly appreciated their attention to detail, clear communication, and proactive approach to identifying opportunities for improvement. I would recommend eCloud Experts to any business looking to improve the accuracy and efficiency of their Xero accounting system.” Ross Becko Director Little Spring Wonders Daycare Nursery Limited About eCloud Experts eCloud Experts is a Xero Gold Champion Partner specialising in Xero Cleanup Services, Xero Health Checks, Xero Optimisation, Xero Bookkeeping Reviews, and complex accounting software migrations. Our team helps businesses identify errors, improve bookkeeping processes, optimise Xero, and ensure that financial reports can be trusted. Whether you need a complete Xero cleanup, a one-off health check, or ongoing support, we